SARS published an EXTERNAL BUSINESS REQUIREMENT SPECIFICATION (BRS) on 28 January 2026 in preparation for implementation. This BRS describes the requirements for a Domestic Constituent Entity (DCE) to submit a GloBE Information Return (GIR) in data file format to SARS. A DCE will build its systems and processes according to these specifications to produce an acceptable XML data file to provide to SARS. The BRS document is a lengthy 214 pages explaining the requirements and means by which such returns are compiled and submitted for processing by SARS.

Previous articles were published on www.fincor.co.za discussing the Global Minimum Tax and BEPS (Base Erosion and Profit Shifting). The reader is advised to read each of these articles for a clearer understanding of BEPS and GMT and then download and read the relevant legislation, policies and documents listed below.

Previous articles were published on www.fincor.co.za discussing the Global Minimum Tax and BEPS (Base Erosion and Profit Shifting). The reader is advised to read each of these articles for a clearer understanding of BEPS and GMT and then download and read the relevant legislation, policies and documents listed below.

The Organisation for Economic Co-operation and Development (OECD) is an international organisation that works to build better policies for better lives. It draws on more than 60 years of experience and insights to shape policies that foster prosperity and opportunity, underpinned by equality and well-being.

OECD works closely with policymakers, stakeholders and citizens to establish evidence-based international standards and find solutions to social, economic and environmental challenges. From improving economic performance and strengthening policies to fight climate change to bolstering education and fighting international tax evasion, the OECD is a unique forum and knowledge hub for data, analysis and best practices in public policy. Its core aim is to set international standards and support their implementation – and help countries forge a path towards stronger, fairer and cleaner societies.

Pillar Two Model Rules (also referred to as the “Global Anti-Base Erosion” or “GloBE” Rules), released on 20 December 2021, are part of the Two-Pillar Solution to address tax challenges due to economic digitalisation and were agreed upon with 140 member jurisdictions of the OECD / G20 Inclusive Framework on BEPS.

This project is to ensure that large Multinational Enterprises (MNEs) pay a minimum level of tax on the income arising in each jurisdiction where they operate. Taxpayers in scope calculate the effective tax rate for each jurisdiction where they operate and pay a Top-up Tax for the difference between their effective tax rate per jurisdiction and the 15% minimum rate. Any resulting Top-up Tax is generally charged in the jurisdiction of the Ultimate Parent of the MNE. A de minimis exclusion applies where there is a relatively small amount of revenue and income in a jurisdiction.

References to Legislation, Policies and Documents

Government Gazette Act No. 46 of 2024: Global Minimum Tax Act, Act 2024.

Government Gazette Act No. 47 of 2024: Global Minimum Tax Administration Act 2024.

National Treasury Draft Explanatory Memorandum on the Global Minimum Tax Bill, 2024 – 21 February 2024.

OECD GloBE Information Return (Pillar Two) XML Schema – User Guide for Tax Administrations – January 2025.

OECD Tax Challenges Arising from the Digitalisation of the Economy – Multilateral Competent Authority Agreement on the Exchange of GloBE Information (January 2025) – Inclusive Framework on BEPS.

OECD Tax Challenges Arising from Digitalisation of the Economy – Global Anti-Base Erosion Model Rules (Pillar Two) – INCLUSIVE FRAMEWORK ON BEPS – 14 December 2021.

OECD Tax Challenges Arising from the Digitalisation of the Economy – GloBE Information Return (January 2025) Inclusive Framework on BEPS.

OECD GloBE Information Return (Pillar Two) Status Message XML Schema User Guide for Tax Administrations – User Guide for Tax Administrations, July 2025.

OECD Tax Challenges Arising from the Digitalisation of the Economy – Consolidated

Commentary to the Global Anti‑Base Erosion Model Rules (2025) Inclusive Framework on BEPS.

SARS SARS_GMTDataFileV1.2 – XML Schema.

SARS Excel spreadsheet GloBE_XML-19.xlsx. Reference GLOBE_OECD and GMT_SARS structures.

STRUCTURE OF THE SARS FILE DECLARATION XML SCHEMA

Important Deadlines for the Global Information Return (GIR)

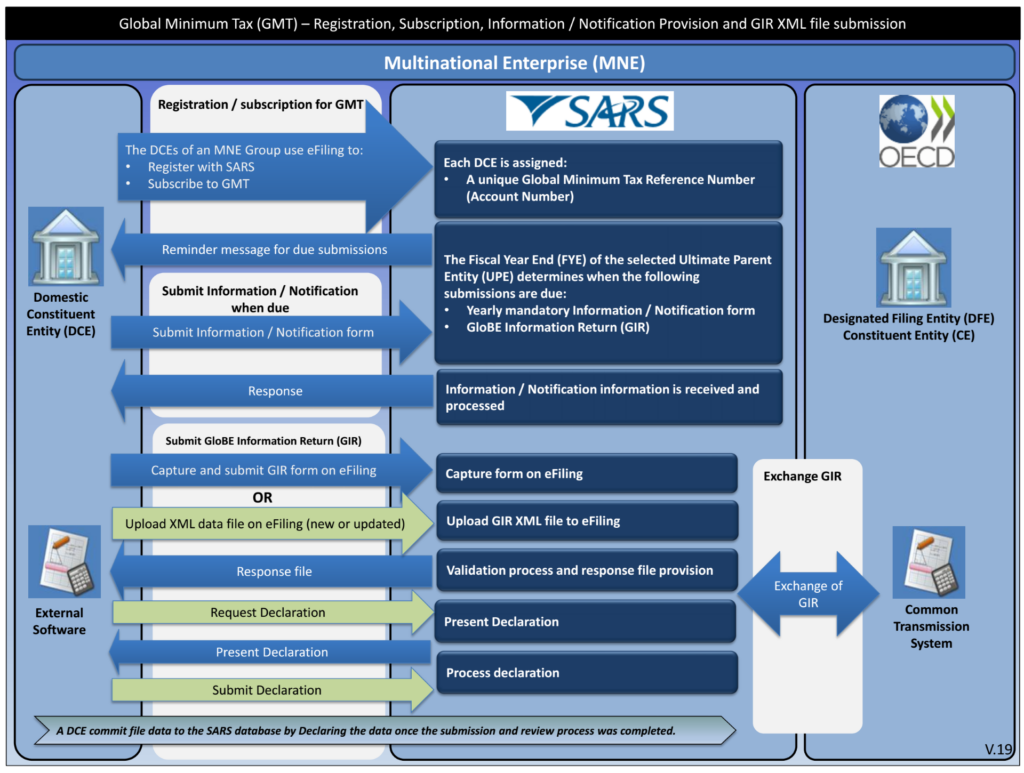

March 2026: The eFiling portal for GloBE registration and notification goes live.

30 April 2026: Extended deadline for notifying SARS who will file the GIR (Designated Local Entity, Ultimate Parent Entity, or Designated Filing Entity).

30 June 2026: Extended deadline for submitting the GIR for MNE Groups with fiscal years ending before 31 December 2024.

For other MNEs: GIRs must be filed 18 months after the end of the 2024 fiscal year (and 15 months for future years).

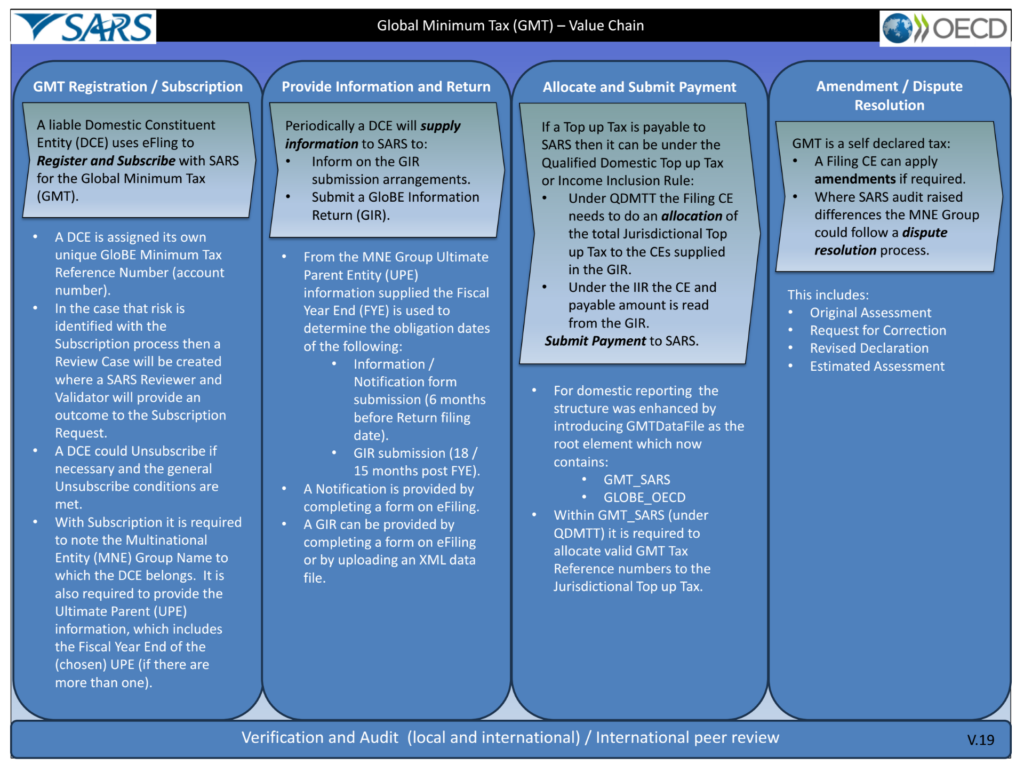

The GIR is a mandatory new filing that shows how much tax the MNE group paid in each country. It helps SARS check if the global minimum tax rule is being followed.

South African entities in the group must either file the GIR locally or notify SARS which in the group will do so (in which country) and confirm that country has a proper agreement in place with South Africa for automatic information sharing.

For domestic reporting purposes, SARS mainly makes use of the OECD-provided schema. Article 9(1) of the GMTA excludes the allocation of Top-Up Tax under the QDMTT. To provide the industry with a mechanism to report to SARS, who must pay Top-Up Tax, a new element called GMT_SARS was introduced.

The main sections of the GMT_SARS Schema are:

I. Contact Details;

II. Tax Details where the Filing CE allocates the total amount of Jurisdictional Top-up Tax to the Constituent Entities (CEs) as provided in the GLOBE_OECD structure.

The main sections of the GLOBE_OECD Schema are:

I. The Message Header with the sender, recipient, message type and Reporting Fiscal Year;

II. The ID and TIN types, used for providing identifying and TIN information in relation to CEs, JVs, JV subsidiaries and UPEs.

III. The GloBE Body, which contains five sub-sections:

a. Filing Info, which contains information identifying the Filing CE and MNE Group;

b. General Section (NB the scope of the term is limited in comparison with the definition under the GIR MCAA), which contains information on the corporate structure of the MNE Group;

c. Summary, which contains the high-level summary of GloBE information;

d. Jurisdiction Section, which contains information on the relevant safe harbours and exclusions, ETR computations, Top-up Tax computations where necessary, and finally the allocation of Top-up Tax, if any; and

e. UTPR Attribution, which contains information on the attribution of Top-Up Tax amongst relevant jurisdictions in case the UTPR is applicable.

The requirement field for each data element and its attribute indicates whether the element is validation or optional in the schema. Every element is one or the other in the schema.

“Validation” elements MUST be present for ALL data records in a file, and an automated validation check can be undertaken. The Sender should do a technical check of the data file content using XML tools to make sure all

“Validation” elements are present, and if they are not, correct the file. The receiver may also do so and, if incorrect, may reject the file. Where there is a choice between two validation elements under a validation parent, and only one is needed, this is shown as “Validation (choice)”.

There may be different business rules for elements that are optional in the schema:

- Some optional fields are shown as “Optional (Mandatory)” – an optional element that is required to be completed whenever the GloBE Model Rules require its completion. Mandatory elements may be present in most (but not all) circumstances, so there cannot be a simple IT validation process to check these. For instance, the IntShippingIncome element must only be completed in cases where the International Shipping Income exclusion applies (i.e., when the MNE Group has International Shipping Income).

- Optional elements may be provided, but are not required to be completed.